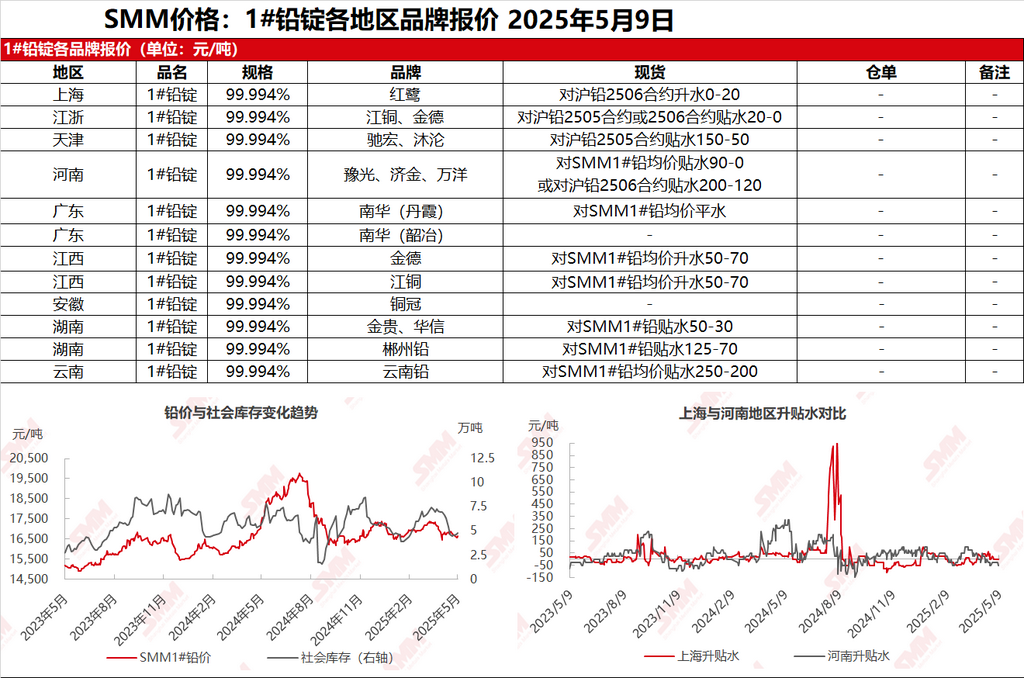

SMM, May 9: In the Shanghai market, Honglu lead was quoted at 16,750-16,780 yuan/mt, with premiums of 0-20 yuan/mt against the SHFE lead 2506 contract. In Jiangsu and Zhejiang regions, JCC and Jinde lead were quoted at 16,730-16,780 yuan/mt, with discounts of 20-0 yuan/mt against the SHFE lead 2505 contract or the 2506 contract. SHFE lead maintained a consolidation trend, with suppliers shipping goods at market prices. Some quotations saw a further widening of discounts, particularly for cargoes self-picked up from production sites at smelters, which were quoted at discounts of 125-0 yuan/mt against the SMM 1# lead price ex-factory. In the secondary lead sector, smelters reduced their shipments, with some secondary refined lead quotations at discounts of 50-0 yuan/mt against the SMM 1# lead average price. Downstream enterprises made just-in-time procurement only, with significant bargaining, and some transactions were concluded for cargoes with expanded discounts.

Other markets: Today, the SMM 1# lead price remained unchanged from the previous trading day. In Henan, quotations for cargoes self-picked up from production sites at smelters widened to discounts of 50-90 yuan/mt against the SMM 1# lead price ex-factory. In Hunan, smelters' quotations were at discounts of 50 yuan/mt against the SMM 1# lead average price ex-factory, while traders' quotations widened to discounts of 125-70 yuan/mt against the SMM 1# lead average price. In Guangdong, quotations for cargoes self-picked up from production sites were adjusted downwards to parity with the SMM 1# lead average price ex-factory. Lead prices gradually stabilized, with suppliers shipping goods at expanded discounts. Downstream enterprises purchased at low prices as needed, and regional transactions in the spot market improved relatively.